BLOG

The Benefit of Bad News

During every bull market, there is no shortage of commentators predicting the imminent end of the rally. These bearish forecasts often receive significant media attention, fueled by concerns over geopolitical conflicts, including the war with Iran, inflation, tariffs, rising living costs, a sluggish residential real estate market, elevated gasoline prices, high mortgage rates, and the latest comments or policies coming from Washington.

These concerns have had an unusual impact on consumer sentiment. According to the University of Michigan Consumer Sentiment Survey, consumer optimism has remained near its lowest levels since 1972, when the University started tracking consumer sentiment.

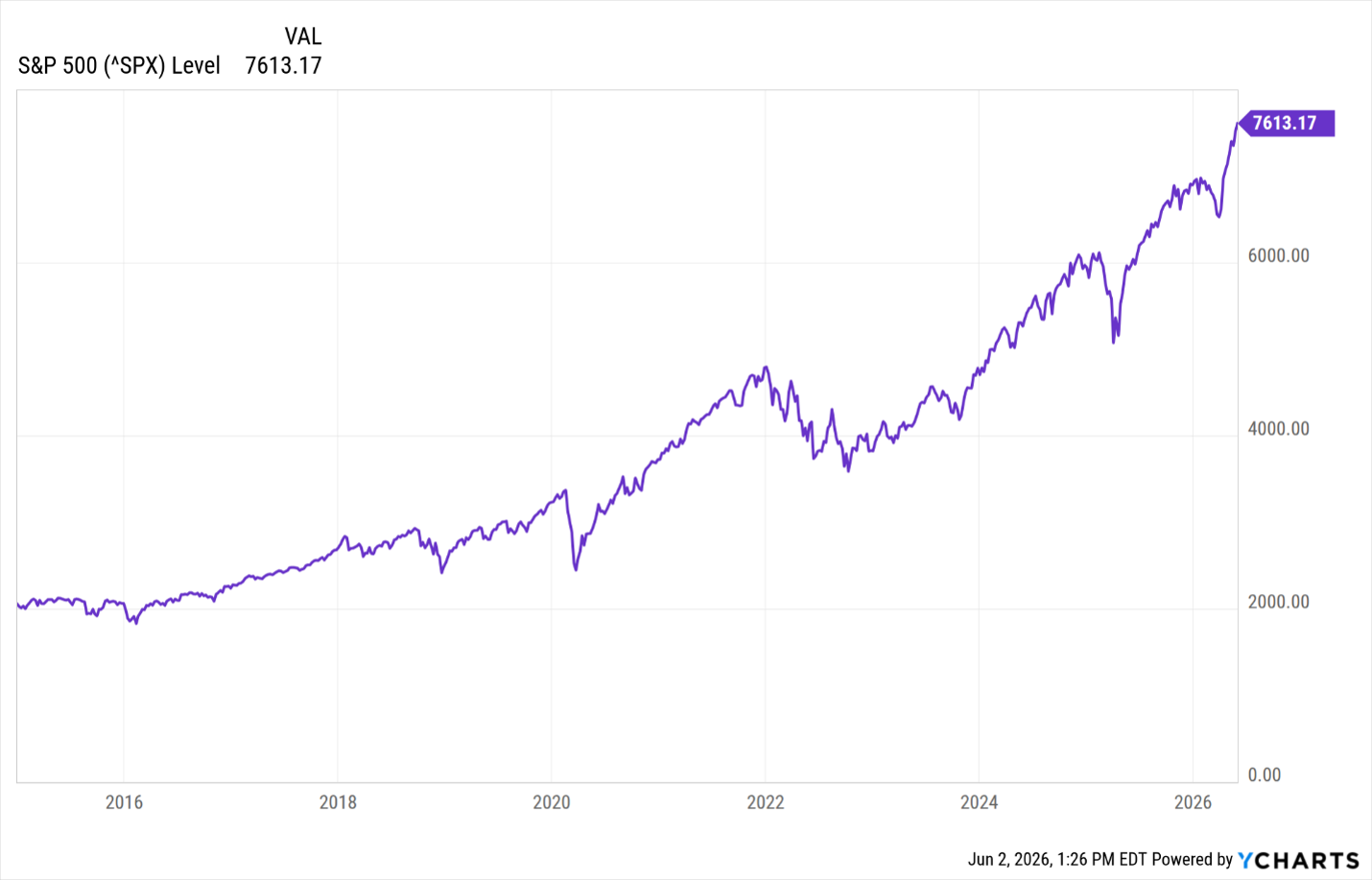

Meanwhile, the stock market continues to advance and periodically records new all-time highs (ATHs). So far in 2026, the S&P 500 has recorded only two new ATHs. However, that follows a robust 57 new ATHs in 2024 and 38 in 2025. New all-time highs during periods of economic expansion and growing corporate profits are not unusual; they are a hallmark of long-term bull markets.

Historically, economic growth and market expansion cycles have often lasted 14 to 17 years and are characterized by a sustained upward trend punctuated by recurring new all-time highs. Based on this framework, I identify the current growth cycle as having begun in 2014. While periods of volatility and market corrections are inevitable, the longer-term trend remains positive as evidenced by the market's ability to continue reaching new highs.

The chart below illustrates the performance of the S&P 500 from January 1, 2015, through yesterday and highlights the persistence of this ongoing growth cycle.

The market environment and investor behavior are markedly different during Contraction/Recession cycles. For comparison, from 2000 through 2012, the S&P 500 recorded only two new all-time highs during this 13-year period. This extended timeframe was characterized by the bursting of the technology bubble, the financial crisis, and a prolonged recovery that left investors uncertain about the market's long-term direction.

As the Contraction/Recession cycle began to end, the S&P 500 entered a typical strong recovery phase during 2013 and 2014 to lead into the next Growth/Expansion cycle. During this latter stage, investor confidence improves, economic conditions stabilize, and corporate profits resume their upward trajectory of improving sales and net profits. During these latter two years alone, the index recorded 103 new all-time highs, signaling a transition from recovery to a sustained Growth/Expansion cycle.

Notice the distinct difference in the chart pattern of the S&P 500 from 2000 through 2014 compared to the chart of the current cycle illustrated above. Rather than the persistent upward slope characteristic of a Growth/Expansion cycle, the market during the Contraction/Recession period exhibited a pronounced "W" pattern, with significant rallies followed by steep declines that often erased much of the prior gains. The scarcity of new all-time highs reflected a market lacking a sustained trend and investors struggling to gain confidence in the future direction of the economy and corporate earnings.

So why can bad news actually be healthy during a Growth/Expansion cycle?

A sustainable bull market requires a balance between buyers and sellers. Buyers represent optimism about future economic growth and corporate profits, while sellers provide skepticism and discipline. Without this balance, stock prices can become either excessively depressed relative to earnings or inflated to unsustainable levels.

Historically, companies in the S&P 500 have traded at approximately 15 to 16 times trailing earnings and 16 to 17 times forward earnings. While current valuations remain above these long-term averages, they are still well below the extremes reached during the technology bubble of 2000. Investors continue to assign premium valuations to companies expected to benefit from artificial intelligence, cloud computing, and other productivity-enhancing technologies.

Bad news serves an important purpose in the market. It challenges investor convictions, encourages caution, and restrains excessive buying enthusiasm. This healthy tension between optimistic buyers and skeptical sellers helps support a more durable and sustainable upward trend.

One of the defining characteristics near the end of a Growth/Expansion cycle is the disappearance of that balance. Investors become increasingly convinced that stock prices can only move higher, causing valuations to detach from underlying fundamentals. Speculation replaces analysis, and companies with compelling stories but little or no profits can attract enormous investor interest. This stage is often described as a market "going parabolic," where certain stocks can experience daily gains of 50% to 100% driven primarily by investor enthusiasm rather than business performance.

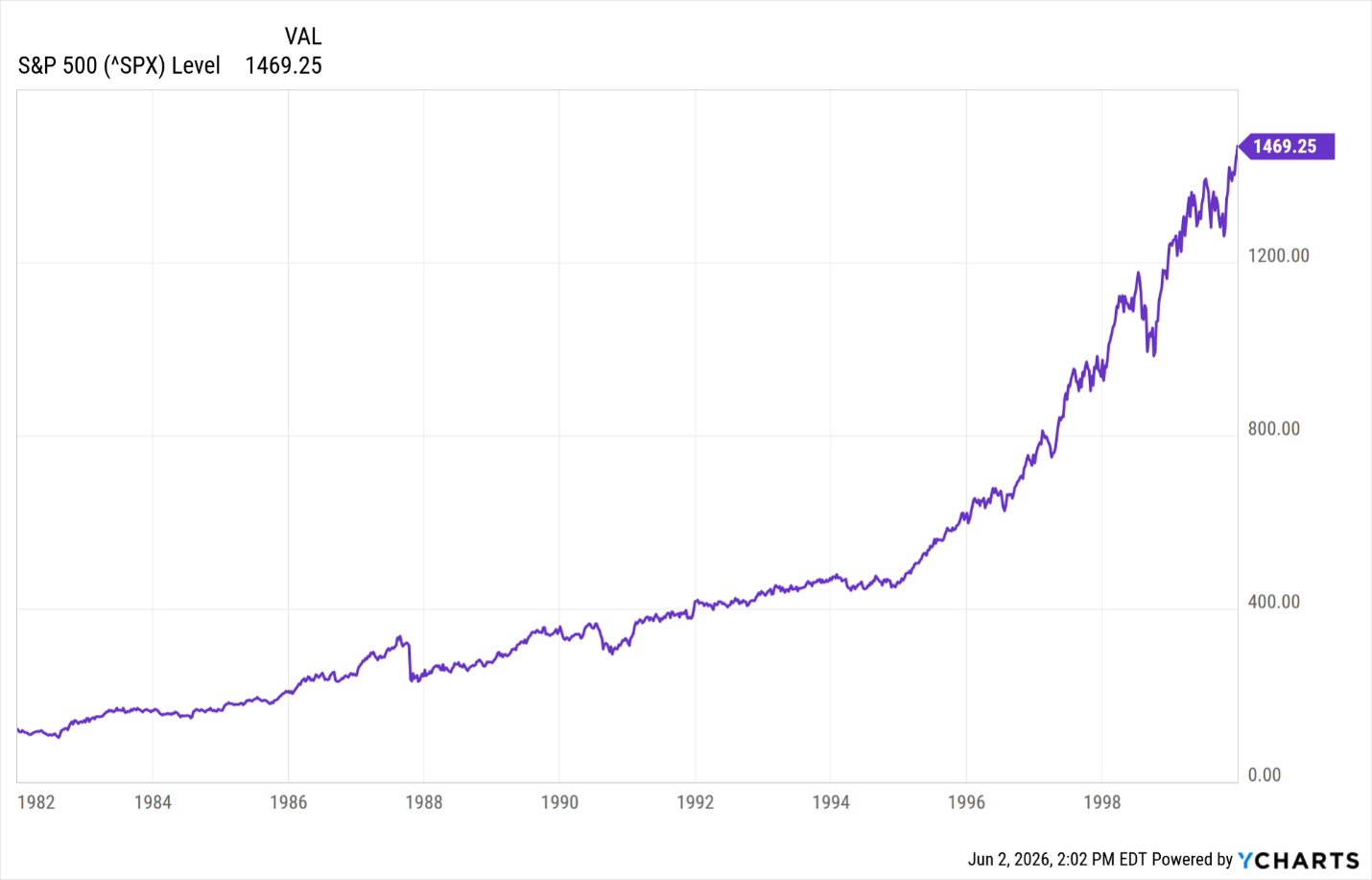

Some investors may look at the current market and conclude that we have already entered a parabolic phase. However, the S&P 500 remains on a path that is similar to the later years of previous Growth/Expansion cycles. Consider the last major Growth/Expansion cycle from 1982 through 1999. During its final five years, the S&P 500 gained more than 220%, produced five consecutive annual returns exceeding 21% (37.6%, 23.0%, 33.4%, 28.6%, and 21.0%), and recorded approximately 288 new all-time highs.

Those who remember the late 1990s will recall the speculative excesses that emerged near the end of that cycle. Many start-up companies with little or no revenue saw their stock prices double on the first day of trading following their initial public offerings. While today's market has certainly benefited from enthusiasm surrounding artificial intelligence and related technologies, the broader market has not yet exhibited the same degree of speculative behavior that characterized the final stages of the dot-com era.

Below is a chart of the S&P 500 from 1982 through 1999. It was an amazing era for investors, but not unusual during Growth/Expansion cycles, as we are experiencing again in this current cycle.

What Does This Mean to Me?

We maintain our positive outlook on the U.S. economy and stock market. Periodic market pullbacks and corrections continue to provide attractive buying opportunities for investors. However, this is not a blanket strategy that applies to every stock. Many sectors and individual companies have not participated in the current Growth/Expansion cycle, and some continue to struggle with stagnant sales, declining earnings, or unfavorable industry trends.

Ultimately, rising stock prices are supported by growing sales, expanding profit margins, and increasing net earnings. Companies that fail to deliver these results often experience selling pressure as investors reallocate capital to businesses with stronger growth prospects.

Successful investing requires ongoing research and discipline. Investors should evaluate individual companies, industries, and sectors to determine whether they are benefiting from sustainable trends that can support future earnings growth. Equally important is the participation of institutional investors. Large pension funds, mutual funds, hedge funds, and other institutional investors control trillions of dollars in assets and are often the driving force behind sustained stock price appreciation. Increasing trading volume accompanied by rising stock prices can be an indication that these investors are accumulating shares and reinforcing the positive trend.

Without continued earnings growth and institutional support, even promising companies can struggle to achieve meaningful stock price appreciation. Identifying businesses with both strong fundamentals and growing investor sponsorship remains a key component of successful long-term investing.

Give us a call or schedule a time we can discuss your goals and investing strategy. We welcome the opportunity to assist you and your family in achieving your financial objectives.

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2026 | Privacy Policy | Terms & Conditions