BLOG

Investors Not Panicking

On June 12–13 of last year, Israel carried out large-scale airstrikes against Iran, targeting nuclear facilities, military bases, and senior commanders and scientists. Dozens of sites were neutralized, and several top Iranian military leaders were killed.

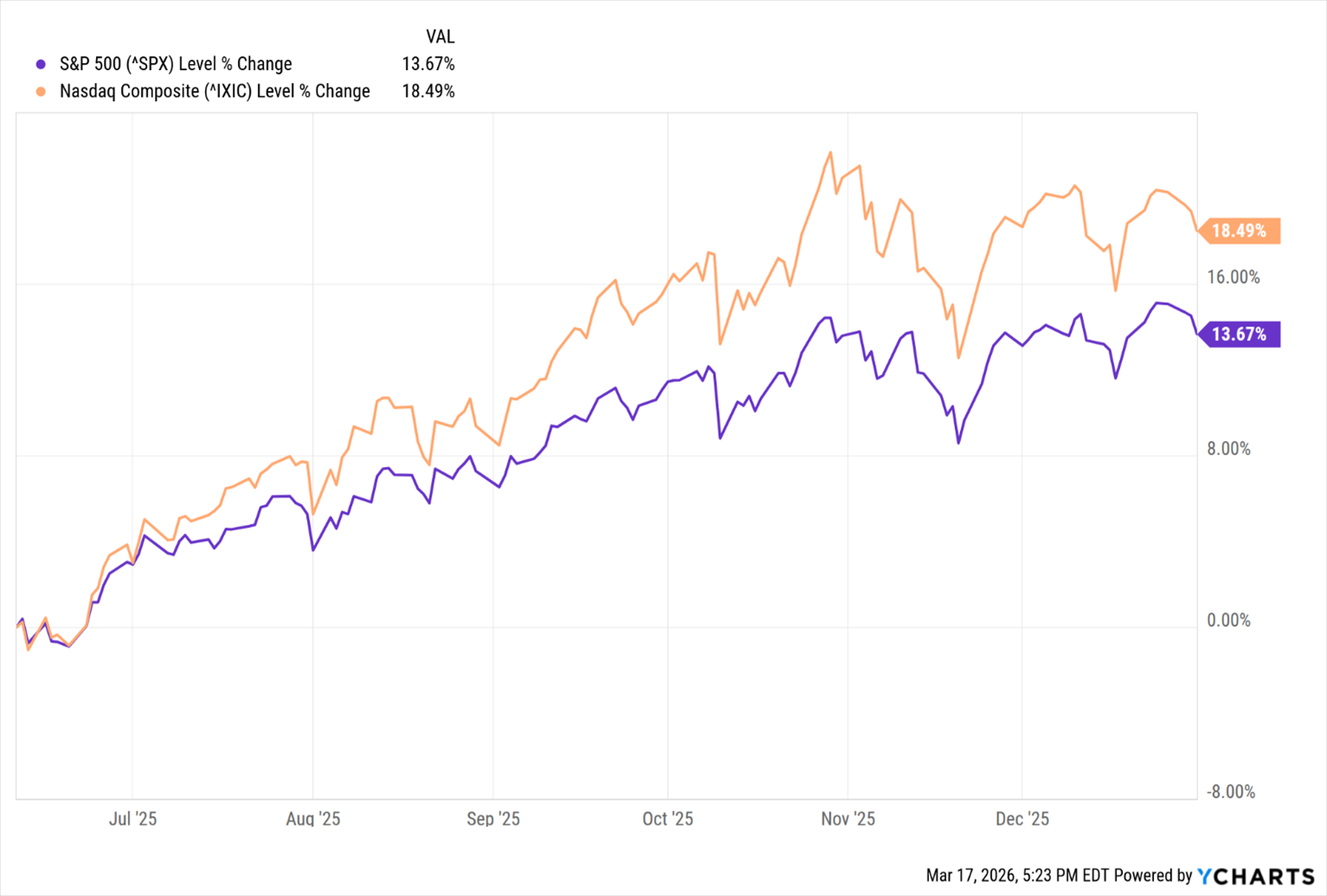

Despite the escalation, U.S. institutional investors showed little concern and continued deploying billions into equities, private equity, and venture capital. Markets responded positively, with both the S&P 500 and NASDAQ reaching new all-time highs. From June 12 through year-end, the S&P 500 rose 13.24%, while the NASDAQ gained 18.20%.

Meanwhile, another group of investors took the opposite approach, allocating capital toward defensive assets such as gold and silver as a hedge against a weakening dollar and potential recession. In an unusual divergence, both risk-on assets—like tech and growth stocks—and traditional safe havens rallied simultaneously.

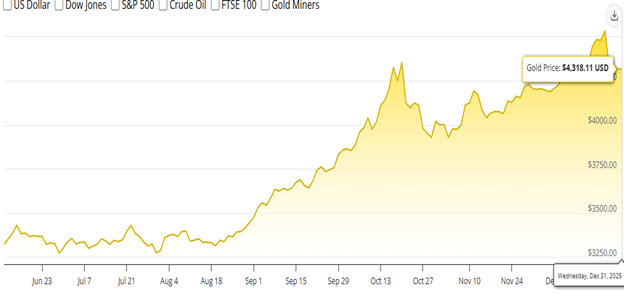

On Wednesday, June 11, 2025, the spot price of gold closed at $3,355.28 per ounce. Following the onset of Israel’s strikes, demand for the metal surged, driving prices up 28.7% by year-end, with gold closing at $4,318.11.

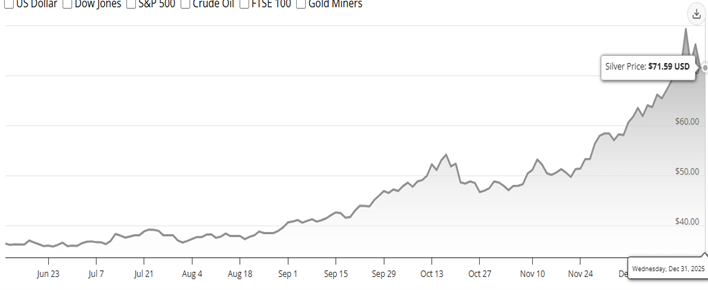

However, the gold rally was mild compared to silver. On June 11, 2026, the silver spot price was $36.24 per oz, and by the end of the year, it had soared 97.5% to close on December 31, 2025, at $71.59 per oz.

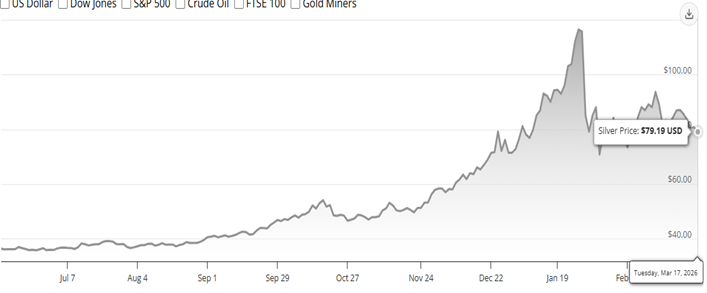

Gold and silver continued to rally into 2026 until they peaked on January 27, 2026. On that day, gold reached its all-time high of $5,414 and silver peaked at $116.61 per oz. Since that day, the precious metals have corrected about 30% of their gains, and metal traders seem ambivalent about the future of the metals market.

We added gold and silver miners to our Growth & Income and Growth Model portfolios in August 2025, which delivered strong gains for client accounts. Our positioning was driven by a range of economic and geopolitical uncertainties, including policy unknowns under the Trump administration, immigration and ICE enforcement dynamics, tariff pressures, a weakening U.S. dollar, and the potential for an expanding conflict with Iran. While many of these issues remain unresolved, the relatively muted response from institutional investors so far this year suggests confidence that these risks are manageable and that a near-term path to resolution is achievable.

More recently, the modest rebound in gold and silver following their correction suggests that upward price momentum has begun to fade, shifting the risk-reward balance. In response, we have taken profits by reducing our exposure to gold and silver mining equities by 50%, with the intention of fully exiting these positions if momentum continues to weaken or reverse. We are glad to be mostly off the merry-go-round of volatile precious metal prices that can end as quickly as they started.

Perhaps the biggest surprise to analysts and media commentators has been the subdued market reaction to the escalation of conflict since June 2025. At the onset of Israel’s strikes, followed by U.S. involvement, many forecasts pointed to negative GDP growth, a potential recession, rising inflation, and job losses.

Despite these concerns, major U.S. indices have remained relatively stable year-to-date even in the face of risks comparable to a 1970s-style oil shock, including the potential closure of the Strait of Hormuz and ongoing missile activity targeting key cities such as Tel Aviv, as well as locations in the UAE, Bahrain, and Qatar, alongside U.S. military installations in the region.

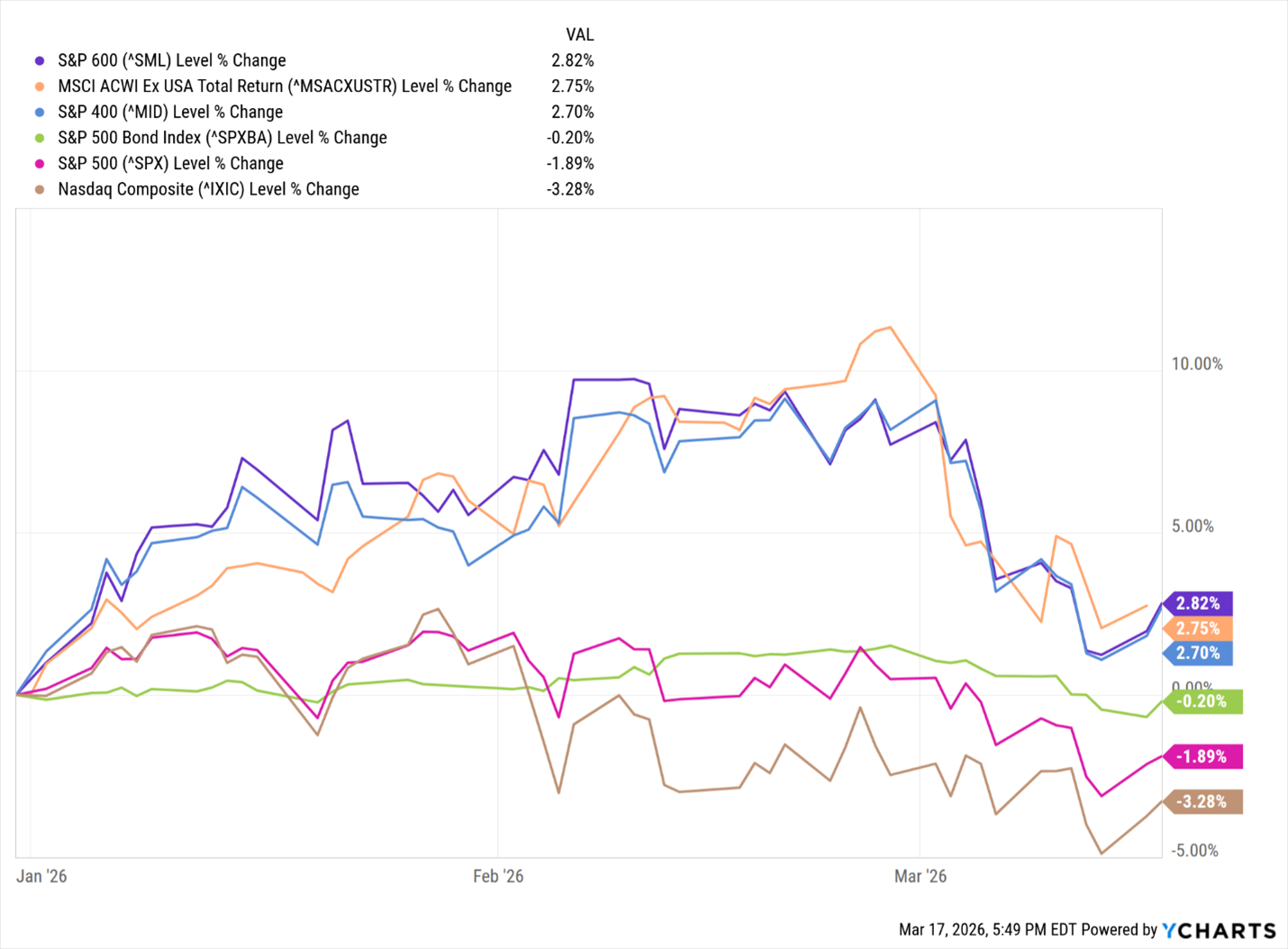

Through today, the major US indices, MSCI Ex US, and bond markets have been very stable. Even though the VIX (S&P 500 volatility index) has increased from a low volatility level of 14 to an increasing volatility range of 24, the US equity markets have not experienced widespread panic selling days. The S&P 500 is down -1.89% and NASDAQ is down -3.28%.

What Does This Mean to Me?

Other than the recent selling of the gold and silver mining, we have not made additional defensive profit-taking trades. We will be monitoring stock market activity as insight into the directions institutional investors are taking. Should the Iran war end soon, along with the opening of the Strait of Hormuz, we would anticipate the US and foreign equities to rally and precious metals to retreat even more. The Federal Reserve is unlikely to lower rates no sooner than this fall. I candidly don’t understand why the media is so focused on the Fed’s lowering rates other than giving consumers and businesses the opportunity to borrow at lower interest rates. Debt is not an asset and drains net worth with fees and interest charges. It was great obtaining loans at artificially low interest rates of 1% to 2%, but that was hopefully a once-in-a-lifetime situation.

We anticipate market conditions to remain stable until they are not, at which time we will adapt to new market conditions as we have for the past 28 years. Currently, we maintain our favorable view on the US economy and stock markets.

CONTACT

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2024 | Privacy Policy | Terms & Conditions