BLOG

Stocks Need to Rebuild New Uptrend

An uptrend can lose momentum for many reasons. Sometimes, unexpected political, economic, or global events disrupt the market and reverse direction. Other times, a rally simply becomes overextended, with investors searching for an excuse to take profits. In most cases, positive momentum gradually slows before ultimately turning negative.

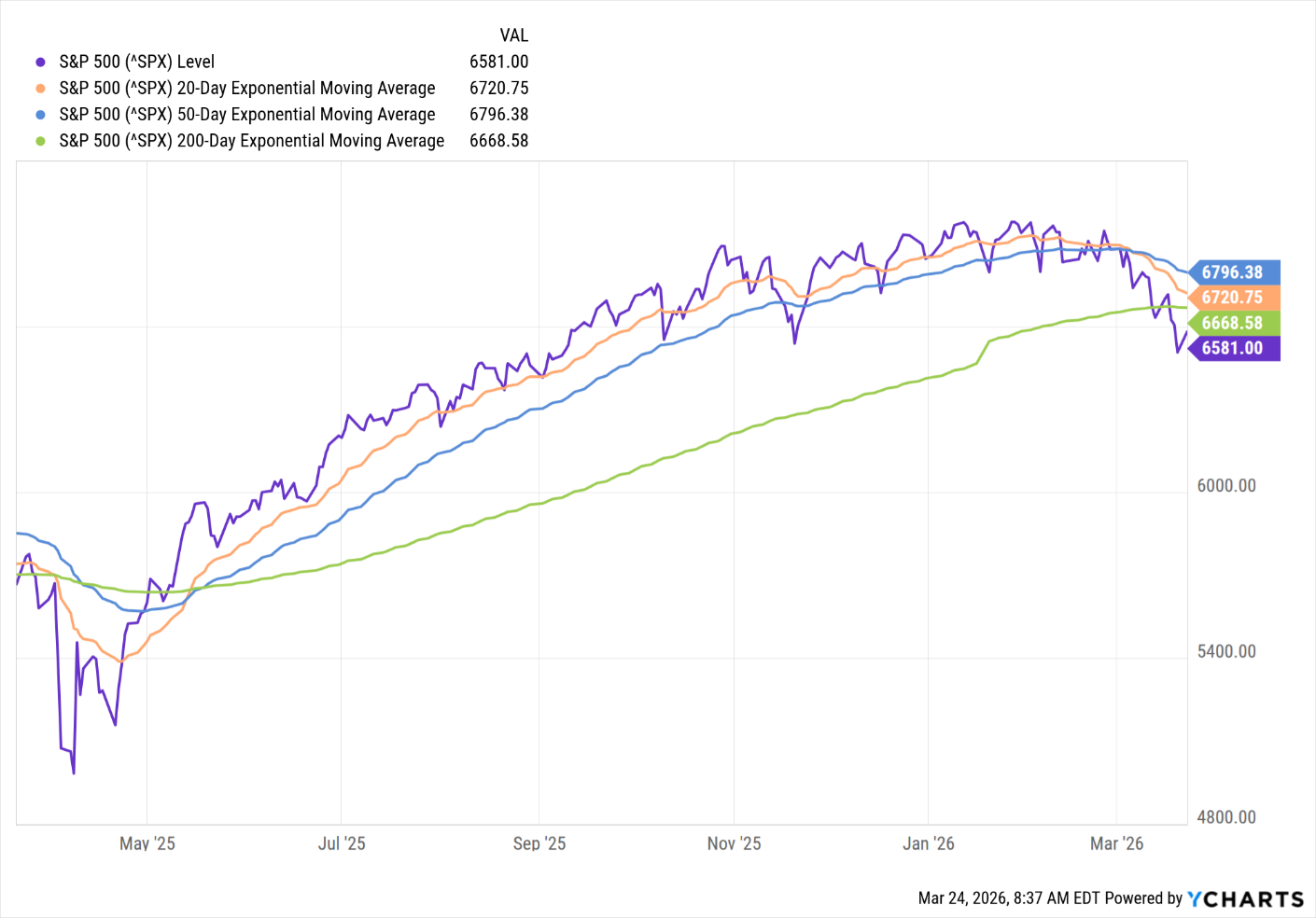

Since peaking on October 28, 2025, the major indices have traded within a narrow range. Well before concerns about war and rising oil prices emerged, institutional investors had already begun reducing their stock accumulation and maintaining a more neutral allocation across stocks, bonds, and cash. Market prices are driven by the balance between buyers and sellers, and when buyers dominate, prices rise; when sellers take over, prices fall. Since late October, trading volume has declined as institutional investors largely remained on the sidelines.

As a result, the S&P 500 lost its upward momentum, reflected in the flattening of the 20-day and 50-day moving averages. Between October 28, 2025, and February 15, 2026, the index briefly moved above these averages multiple times but failed to sustain a breakout. Following renewed military action involving the U.S., Israel, and Iran on February 28, investor sentiment shifted from neutral to negative. Selling pressure began to outweigh buying demand, pushing the S&P 500 below its 20-day, 50-day, and 200-day moving averages.

Despite the potential threat to global commerce if the conflict with Iran spreads, the U.S. stock market has remained relatively stable. Investors do not appear to be pricing in the additional risks of widespread shortages of food or supplies, with similar disruptions seen in 2020. Notably, institutional investors are some of the world’s most informed investors, managing multi-billion-dollar hedge funds, mutual funds, and private equity portfolios. So far, they are not aggressively reducing their equity exposure. Their trading behavior suggests expectations of a near-term resolution to the Iran conflict and a reopening of the Strait of Hormuz.

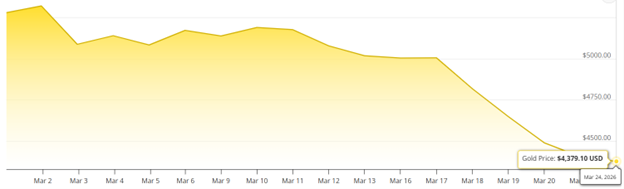

Another notable and somewhat counterintuitive development has been the recent selloff in precious metals and mining stocks even as global risks escalated in February. Historically, gold and silver tend to rise during periods of uncertainty, serving as a hedge against factors such as a strengthening U.S. dollar, rising oil prices, recession fears, geopolitical tensions, and war. However, as these risks intensified, gold and silver prices declined sharply over a short period.

Following the onset of the Iran-related conflict, gold reached a peak of $5,321 per ounce on March 1, but has since fallen approximately 18%, closing yesterday at $4,379.10.

Silver spot price was 89.1 on March 1st and plummeted 23% through yesterday to close at a spot price of $68.24.

Mining stocks declined alongside precious metals. The most plausible explanation for the sharp selloff in gold, silver, and related mining equities is that the strong rally over the past 18 months had already priced in risks such as war and supply chain disruptions. When those events began to unfold in late February, investors appeared to reassess the situation and conclude that the risks were less severe than previously anticipated. While I have great respect for the market and institutional managers, it is difficult to fully accept that this level of foresight was accurately priced in as early as late 2024.

A core component of our portfolio management process is monitoring momentum. By observing institutional investor trading activity, we gain insight into their expectations. While we may not always know the specific reasons behind their decisions, their actions often signal how we should position our own portfolios.

As gold and silver began to decline following their strong 18-month rally that started in late 2024, it signaled to us that the positive trend was beginning to reverse. I did not expect the downturn to be so sharp, especially given the escalating conflict with Iran. At first glance, the pullback could have been viewed as a temporary correction and a potential buying opportunity. However, as selling pressure accelerated, we chose to exit all gold and silver mining positions in our model portfolios over the past 10 days. This decision enabled us to lock in the gains from 2025 and preserve a portion of the profits generated in 2026.

Since then, mining stocks continued to decline until yesterday, when they rebounded following President Trump’s announcement regarding favorable negotiations with Iran (another counterintuitive market reaction). It remains to be seen whether gold, silver, and their related mining stocks can resume their upward trajectory and surpass previous all-time highs of $5,500 and $120 per ounce, respectively.

Over more than 30 years of managing portfolios, I’ve learned, often the hard way, that investing in commodities can be both short-lived and highly risky. Back in 2006, while living in California, I began trading commodities futures in my personal account. My positions included gold, silver, copper, soybeans, corn, cattle, and other contracts. Since the futures market opened at 6:00 a.m. Pacific Time, I was able to trade for a couple of hours before starting my day job as a portfolio manager in San Jose.

At the time, trading was still largely executed on the floor. Orders were relayed by “runners” who physically rushed them to brokers in the trading pits, where trades were shouted back and forth. It was a far cry from today’s digital markets, with some confirmations taking up to 10 minutes. The experience was exhilarating, and on several mornings, I made more than I earned in an entire month at my day job.

However, the warning signs were there early on. I underestimated the substantial risks involved, particularly the extreme leverage embedded in futures contracts that typically represent financial exposure 100 times greater than the initial investment. For example, a single gold contract represents 100 troy ounces, which at recent prices equates to roughly $430,000 worth of gold. Unlike traditional investments, there is effectively no limit to potential losses, and margin calls must be met immediately, often within the same day.

Since February 28, gold prices have fallen by about $1,000 per ounce. If an investor had purchased just ONE gold contract at a cost of about $5,300 late February, the cumulative loss would exceed $100,000, requiring daily capital infusions to cover negative balances over the past several weeks.

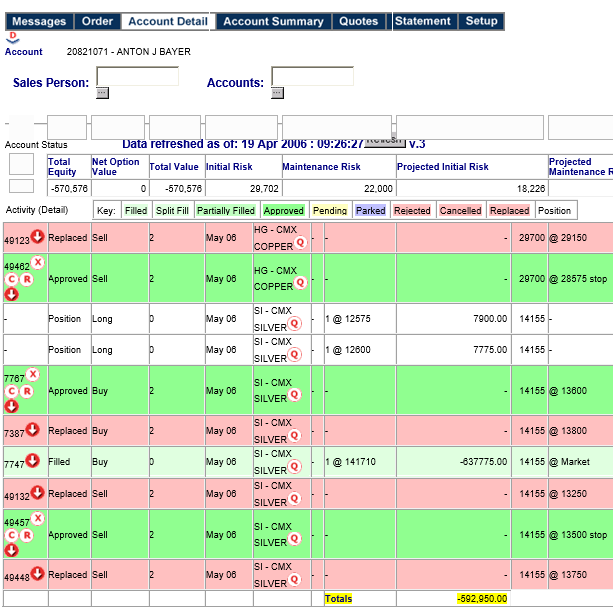

One day during this time of trading, I had placed buy limit orders for TWO silver contracts. Upon logging into my trading account the next morning, the screen immediately turned RED with messages that my account is restricted and to call my trading broker. My account had a negative margin balance of $592,950! See my statement below.

Needless to say, this would have been financially devastating, not to mention the very uncomfortable conversation with my wife. As it turned out, thankfully, someone at the broker's office entered the trade strike price incorrectly (listed in 5 digits with no decimal point), buying silver well over market price, which immediately was a losing position. Hours later, they finally cleared my trade with the broker, paying the $592,950 deficit, and re-enabled my account.

A more logical person would have recognized this as an omen to get out and shut down this nonsense. I, on the other hand, continued to play in this very dangerous market for several more months before liquidating my account with less than my original investment but with my house, family, and livelihood intact.

What Does This Mean to Me?

The trading activity of institutional investors indicates they are not overly concerned with recent developments in the Iran war and other associated risks. In addition to limited concern about unintended consequences of the war, they appear to be content so far with domestic issues that include changes of the Federal Reserve Chairman, rising inflation and interest rates, declining consumer sentiment, changes with tariff tax schedules, and stagnating residential real estate market, to name a few.

Should the conflict with Iran be resolved and the Strait of Hormuz reopened, I would anticipate a short-lived global equity market rally. The continuation of the rally will be predicated on new economic news to add to its momentum. Gold and silver spot prices have been trading in counterintuitive directions, rallying in 2025 along with the US economy and stock market, and declining with the escalation of war. So, it remains to be seen what changes occur with precious metal spot prices as geopolitical challenges are resolved, and global economies begin to recover.

The proceeds from the sale of our gold and silver mining stocks were allocated to a US Treasury Money Fund in our Growth and Growth & Income Model portfolios. We intend to hold these unusually large balances in the Treasury Money Fund until a new positive uptrend is established.

Let us know if you have any questions about this UPdate or about your account. We welcome the opportunity to assist you and your family in achieving your goals.

CONTACT

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2024 | Privacy Policy | Terms & Conditions