BLOG

Differing Moods of Investors and Consumers

Before the war with Iran, both investors and consumers were already facing significant uncertainty about the outlook for their finances and the broader U.S. economy. Investors were focused on several key issues, including the future path of Federal Reserve interest rates, the appointment of a new Federal Reserve Chair, rising inflation, and the potential effects of tariffs.

Consumers, meanwhile, had their own set of concerns. These included persistently high mortgage rates, a sluggish housing market, the rising cost of living, and worries about job security, particularly considering increasing AI-related disruption.

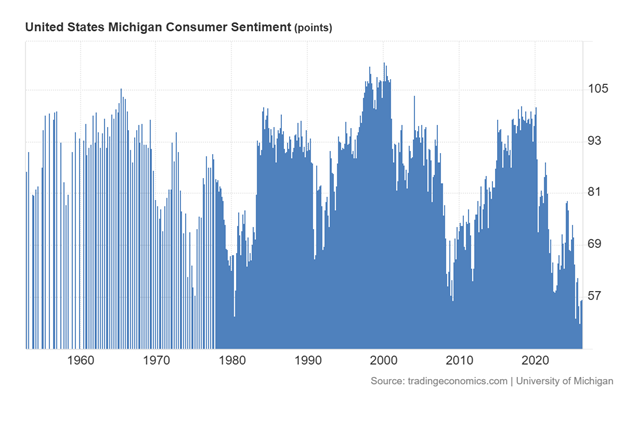

However, consumers are experiencing a greater level of anxiety than business owners. The University of Michigan’s Consumer Sentiment Index fell to 53.3 in March 2026, down from a preliminary reading of 55.5 and below February’s 56.6.

Joanne Hsu, Surveys of Consumers Director, provided this commentary:

“Consumer sentiment fell back 6% this month to its lowest level since December 2025. Declines were seen across age and political party. Consumers with middle and higher incomes and stock wealth, buffeted by both escalating gas prices and volatile financial markets in the wake of the Iran conflict, exhibited particularly large drops in sentiment. Overall, the short-run economic outlook plunged 14%, and year-ahead expected personal finances sank 10%, while declines in long-run expectations were more subdued. These patterns suggest that, at this time, consumers may not expect recent negative developments to persist far into the future. These views are subject to change, however, if the Iran conflict becomes protracted or if higher energy prices pass through to overall inflation. Interviews for this release were collected between February 17 and March 23, with about two-thirds completed after the start of the US military conflict in Iran.”

Ms. Hsu noted that this month’s sentiment reading is the lowest since December 2025. However, looking at the data going back to 1953, consumer sentiment has rarely been this depressed and is now dropping to historic lows, only previously reached in April 1980 and during the summer of 2022.

Since February 2020, consumer sentiment has declined sharply, and rebounds have been unusually brief, typically followed by further drops to new lows.

The war has added more uncertainty for both investors and consumers. However, again, consumer sentiment declined at a greater rate than business sentiment. We wrote in our February 11, 2026, update that.

“The National Federation of Independent Business (NFIB) February sentiment index surged to 105.1, its highest level since 2020. Historically, readings above 100 signal solid optimism among small business owners.”

So far, U.S. businesses and consumers have largely remained on the sidelines, with global events having minimal direct impact. Supply chains for most essential goods have stayed intact, and gasoline prices have remained relatively stable—aside from California, where price pressures are driven by factors unrelated to the war. This stability is largely due to the U.S. aggressive expansion in oil and gas production during the past decade, which led the country to become a net exporter of oil and natural gas for the first time in decades in 2019.

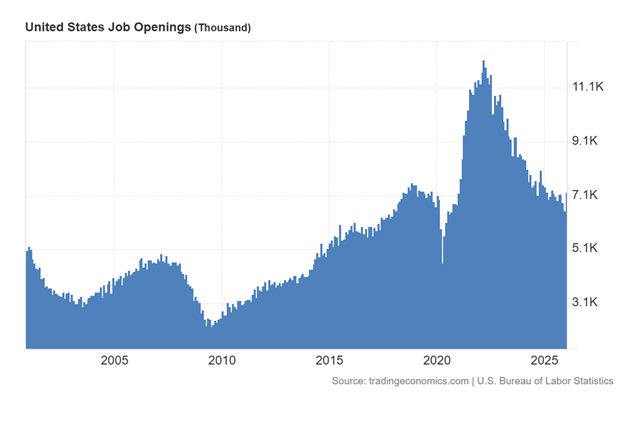

Today, the U.S. Bureau of Labor Statistics (BLS) released its Job Openings and Labor Turnover Survey (JOLTS). In February, hiring and layoffs showed little change, and there was also no significant movement in quits or discharges. The BLS noted the following:

“The number of job openings was little changed at 6.9 million in February, the U.S. Bureau of Labor Statistics reported today. Over the month, hires decreased to 4.8 million, and total separations changed little at 5.0 million. Within separations, quits (3.0 million) were little changed, while layoffs and discharges (1.7 million) were unchanged.

This release includes estimates of the number and rate of job openings, hires, and separations for the total nonfarm sector, by industry, and by establishment size class. Job openings include all positions that are open on the last business day of the month. Hires and separations include all changes to the payroll during the entire month. “

One explanation for the stable number of job openings is the slowing activity of new hires, discharges, and quits. The BLS noted in this month’s report the following:

“The number of hires decreased to 4.8 million (-498,000) in February and was down by 387,000 over the year. The hires rate decreased over the month to 3.1 percent. This was the lowest hires rate since April 2020 when it was also 3.1 percent. In February, the number of hires decreased in accommodation and food services (-178,000) and in construction (-88,000).

In February, the number and rate of quits were little changed at 3.0 million and 1.9 percent, respectively. The number of quits decreased in accommodation and food services (-119,000), wholesale trade (-35,000), and federal government (-6,000). Quits increased in nondurable goods manufacturing (+21,000).

The number of layoffs and discharges remained unchanged at 1.7 million. The layoffs and discharges rate was little changed at 1.1 percent. The number of layoffs and discharges increased in retail trade (+72,000). Layoffs and discharges decreased in nondurable goods manufacturing (-26,000) and in federal government (-3,000).”

Looking at this data going back to 2000, the pre-pandemic peak in job openings occurred in January 2019 at 7.5 million, compared to 6.882 million in February. The lowest level was recorded in July 2009, when job openings fell to just 2.23 million.

Despite ongoing concerns about layoffs, rising unemployment, and a decline in job availability, the U.S. economy and business environment remain stable and, by historical standards over the past two decades, could be viewed as relatively robust.

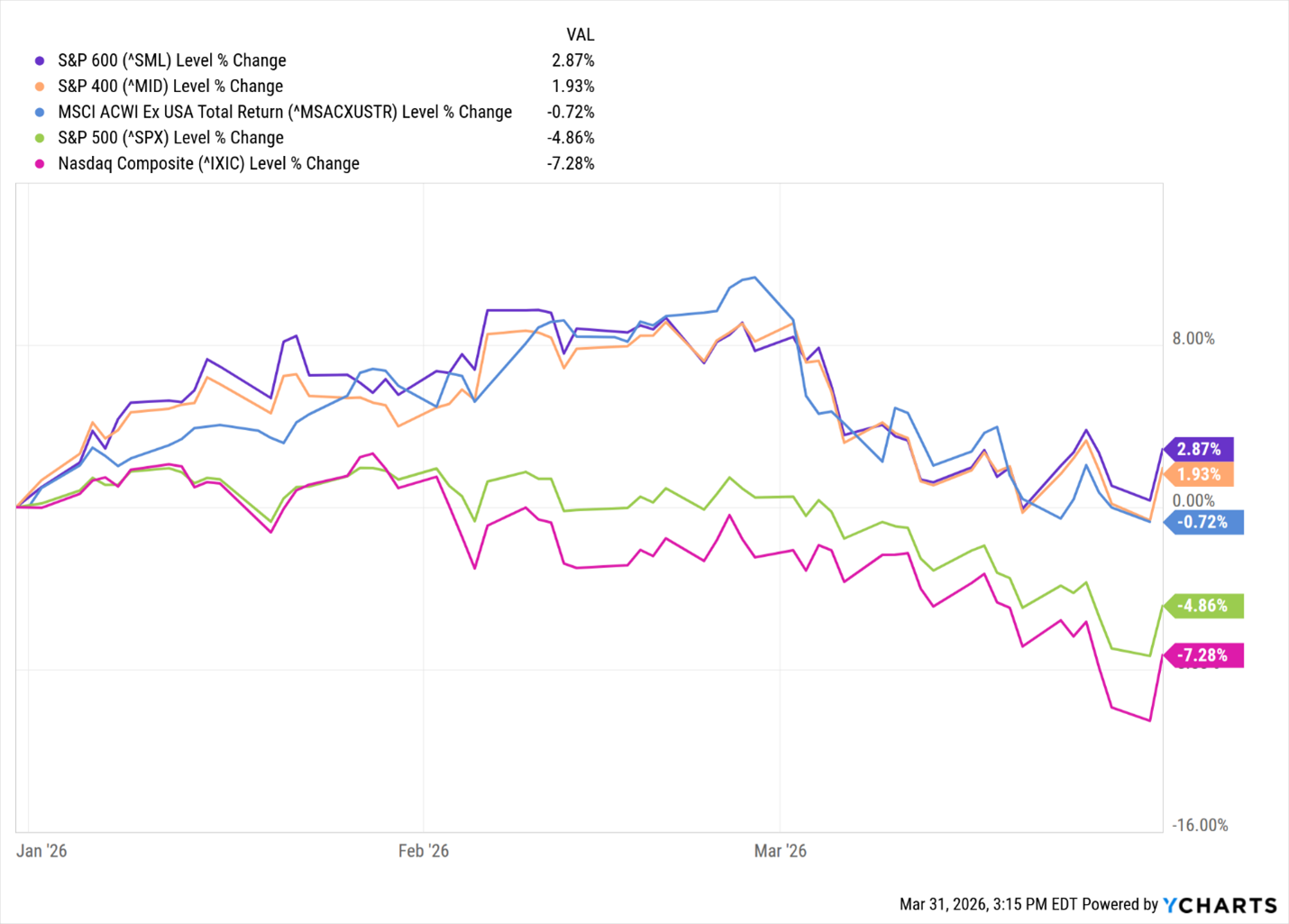

Institutional investors and analysts are expressing concern about contagion with the Iran war impacting supply chains and business growth.

While institutional investors and analysts express concerns about war and domestic issues, the slow net selling of stocks year to date would indicate their much lower level of anxiety. My interpretation of their trading activity is more a concern of FOMO (fear of missing out) than the risks of a continuing selloff. Below is a YTD chart of the major indices. Note the continued leadership of small, mid-cap, and international indices over former leaders of the SP 500 and NASDAQ.

What Does This Mean to Me?

Since early February, we have been increasing cash positions in our Growth and Growth & Income model portfolios. We have not made significant changes to our Income and Balanced portfolios, as they already maintain higher allocations to guaranteed high-yield money market funds and investment-grade bonds.

Within the Growth and Growth & Income models, we began trimming underperforming positions in early February, directing proceeds into cash. As market declines accelerated, we continued this process, bringing cash allocations to approximately 20%. We anticipate a modest rebound in equities and a decline in Treasury yields once a meaningful resolution with Iran is achieved. That may be an opportunity to reinvest the cash allocation in equities.

Today, U.S. equities are experiencing a relief rally driven by optimism around a near-term resolution to the conflict and the potential reopening of the Strait of Hormuz. However, this optimism may prove short-lived, as the rally appears to be based largely on rumors and unofficial commentary from both Washington and Iran. The Strait remains closed, and crude oil prices continue to hover near multi-year highs.

Bloomberg reported today that Iran struck a fully loaded Kuwaiti oil tanker in Dubai waters, raising further uncertainty about Iran’s long-term economic strategy with its Middle Eastern neighbors. Brent crude rose approximately 5% to $118 per barrel, while U.S.-based West Texas Intermediate (WTI) increased about 1% to $101 per barrel.

Our outlook on the U.S. economy and equity markets remains modestly positive. We expect a meaningful rebound in stocks following a sustainable resolution to the Iran conflict and the reopening of the Strait. However, we anticipate that markets may gradually weaken thereafter as attention shifts back to underlying economic challenges. A key variable will be the normalization of energy prices. Historically, CEOs raise prices in increments of dollars with the onset of risks and lower them in increments of pennies as risks are mitigated. It may take several months or longer before retail gasoline prices return to pre-war levels.

This slow realignment of prices may extend across many industries, as business leaders maintain elevated pricing to recover prior profit losses. Unfortunately, higher prices such as the now-common $20 breakfast may persist.

Institutional investors will be closely watching upcoming earnings reports and forward guidance to shape portfolio strategy. From yesterday’s close, the S&P 500 and NASDAQ would need to rally approximately 10% to 16%, respectively, to achieve a 6% gain for the year. While attainable, such gains are unlikely if the war conflict extends through the summer.

We welcome your thoughts on this update. Please feel free to reach out with any questions regarding your investment accounts or financial planning. We look forward to helping you and your family achieve your financial goals.

CONTACT

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2024 | Privacy Policy | Terms & Conditions